Smart Tax Strategies

Tax Planning

Keep more of what you earn through legal, strategic tax optimization. We analyze your income sources, investments, and expenses to implement year-round tax-saving strategies—ensuring you never pay more tax than legally required.

Tax Optimization Strategies

Comprehensive approaches to legally minimize your tax burden

Section 80C & Beyond Planning

Strategically utilize the ₹1.5 Lakh 80C limit across ELSS, PPF, life insurance, and ULIP. We also identify deductions under 80D (health), 80E (education loan), 80G (donations), and 80TTA/80TTB (interest income).

Capital Gains Tax Optimization

Minimize STCG and LTCG through tax loss harvesting, strategic profit booking, and holding period management. We help you utilize the ₹1.25 Lakh LTCG exemption annually and time transactions for optimal tax efficiency.

Salary Restructuring

Optimize your CTC structure to maximize tax-exempt components—HRA, LTA, food coupons, NPS employer contribution, and car leases. A well-structured salary can save ₹50,000-2,00,000 annually in taxes.

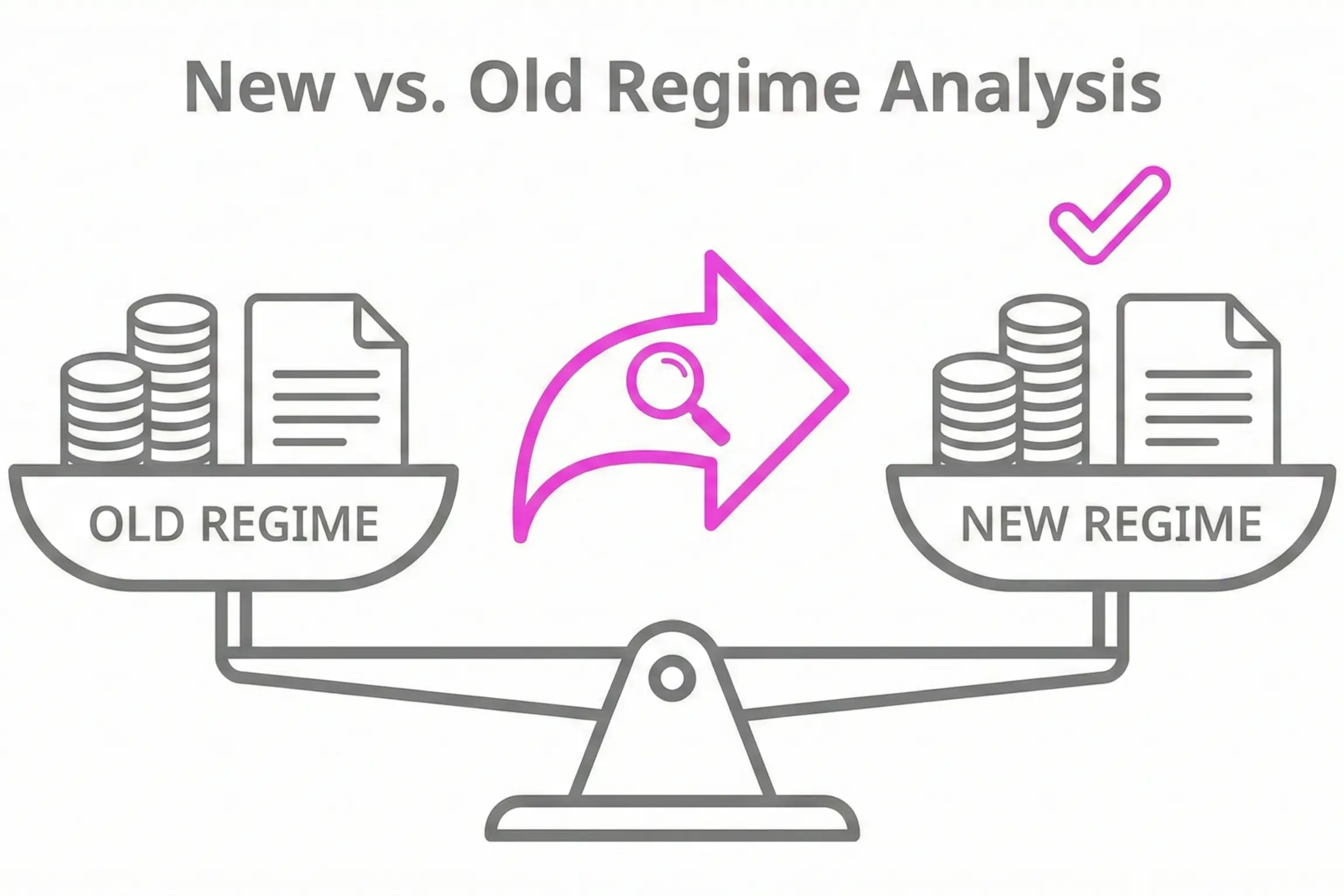

New vs. Old Regime Analysis

Determine which tax regime—new (lower rates, fewer deductions) or old (higher rates, more deductions)—is optimal for your situation. We run detailed calculations annually as your income and deductions change.

NPS & Retirement Tax Benefits

Leverage additional ₹50,000 deduction under 80CCD(1B) through NPS contributions. We integrate NPS into your retirement and tax strategy, considering the 60% lump-sum withdrawal tax treatment.

Business & Professional Tax Planning

For business owners and professionals—optimize through presumptive taxation (44AD/44ADA), maximize deductible expenses, plan advance tax payments, and structure entities for tax efficiency.

Ready to get started?

Our experts are here to guide you through every step of your financial journey.

Frequently Asked Questions

Get answers to common questions about our services.

Experience the impact of expert guidance

Join thousands of intelligent investors who trust i2Finserv for their financial journey.